Energy security and banking stability should get priority

The business community wants to see the government prioritise energy security, banking stability and practical reforms in the upcoming budget for fiscal year 2026-27, Taskeen Ahmed, the president of the Dhaka Chamber of Commerce and Industry (DCCI), has said.

The BNP-led government has inherited a highly challenging economy marked by instability in the energy and banking sectors, high inflation and weak investor confidence, he told The Daily Star in a recent interview.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. He said the upcoming budget should adopt a “realistic” fiscal plan instead of an ambitious one.

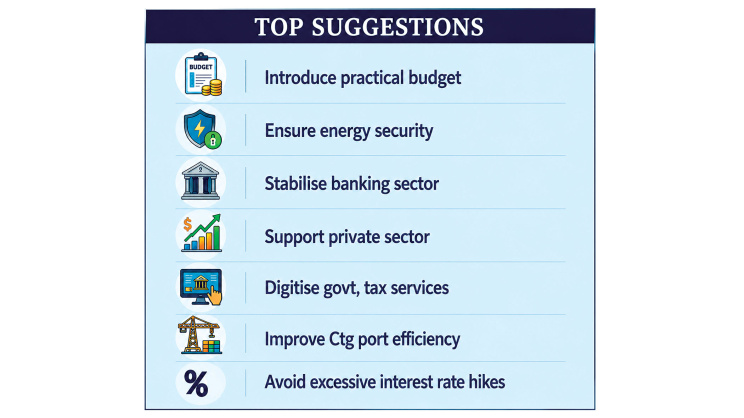

“We are expecting a realistic and practical budget,” he added. “Businesses want to see clear direction and policies that can actually be implemented.”

The ongoing US-Israel war on Iran made things worse, he said, sharply raising Bangladesh’s fuel import costs and injecting fresh uncertainty into global energy markets.

He, however, acknowledged that the “government’s resources are limited” and added that the additional burden of energy imports would force policymakers to make difficult spending decisions in the budget.

He also noted that businesses welcomed some of the government’s early steps, particularly its focus on employment generation, banking reforms and refinancing support for industries.

Rising prices have significantly reduced people’s purchasing power and created a difficult balancing act for policymakers. The current economic situation is close to “stagflation”, where inflation remains high while economic activity slows. Inflation is not falling, but economic activity is slowing down at the same time

ENERGY FIRST

Of all the pressures weighing on businesses, Taskeen was most emphatic about energy.

“Energy security is now more important than the price itself,” he said.

Businesses had accepted repeated increases in energy tariffs over the past few years based on assurances that supply quality and reliability would improve.

“But many industries are still struggling,” he said. “Without an uninterrupted energy supply, production cannot run smoothly, and new investment will remain slow.”

He warned that uncertainty surrounding energy supply was hurting investor confidence at a time when private sector credit growth had already fallen sharply.

“Businesses need confidence to invest,” he said. “That confidence depends heavily on stable energy supply, predictable policies and access to financing.”

He also flagged an uneven energy pricing structure for new industries.

Some newly established plants were being charged higher energy tariffs than older ones operating in the same areas, he said, adding that it is creating an “unequal competition” that was discouraging fresh investment.

STABILISE BANKS

Taskeen also called on the government to focus on reviving the banking sector, describing it as fragile and struggling with liquidity shortages.

With default risks rising and liquidity tight, many banks have grown reluctant to lend, leaving businesses starved of working capital just as private sector credit growth has been falling sharply, said the seasoned businessman, who is also the group vice chairman of IFAD Group.

“Money has to return to the market,” he said. “Banks need to resume lending to productive sectors.”

He argued that businesses genuinely affected by recent shocks -- the Russia-Ukraine war, currency depreciation, rising fuel prices -- deserve temporary policy support to recover.

The government’s early focus on banking reforms and refinancing support for industries was a step businesses had viewed positively, he added.

EXCESSIVE RATE HIKES TO HURT JOBS

On inflation, Taskeen said rising prices had significantly reduced people’s purchasing power and created a difficult balancing act for policymakers.

He described the current economic situation as close to “stagflation”, where inflation remains high while economic activity slows.

“Inflation is not falling, but economic activity is slowing down at the same time,” he said.

He acknowledged that higher policy rates were a globally accepted tool to control inflation but warned against excessive tightening.

“If businesses shut down, people will lose jobs. Then inflation will become an even bigger social problem,” he said.

Supporting businesses should remain a priority because the private sector accounts for around 90 percent of Bangladesh’s GDP, argued the DCCI president.

PRACTICAL REFORMS

Beyond the immediate crises, Taskeen pressed for structural and practical reforms to improve the ease of doing business, particularly through the digitisation of government services and tax administration.

He criticised the requirement for multiple certifications and approvals to start a business, arguing these increased costs and created opportunities for corruption.

Taskeen further stressed the need for reforms at Chattogram port, which handles the majority of the country’s external trade activities.

“Ease of doing business cannot improve unless port operations become faster and more predictable,” he said.

On revenue mobilisation, he said Bangladesh needed to gradually expand its tax net, noting that a large share of economic activity remained outside the formal financial system, limiting the government’s capacity to fund public services.

Restoring business confidence, he said, would require progress across all these fronts together.

“It’s a combination of many factors,” he said. “If the government can ensure energy security, improve banking stability and continue reforms with political commitment, the economy can regain momentum.”

Comments