Bangladesh’s GDP crosses half-a-trillion-dollar mark

Bangladesh’s economy has crossed the half-a-trillion-dollar mark for the first time in fiscal year 2025-26, provisional data from the Bangladesh Bureau of Statistics showed, as better performance in agriculture and services helped regain pace after a sluggish previous year.

The economy grew 4.14 percent in FY26, up from 3.49 percent a year earlier, the BBS said while releasing the estimate for the year ending June 30.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. The agency made the estimate based on data from the first three quarters till March and will be revised again once the year ends, one official familiar with the process told The Daily Star on condition of anonymity.

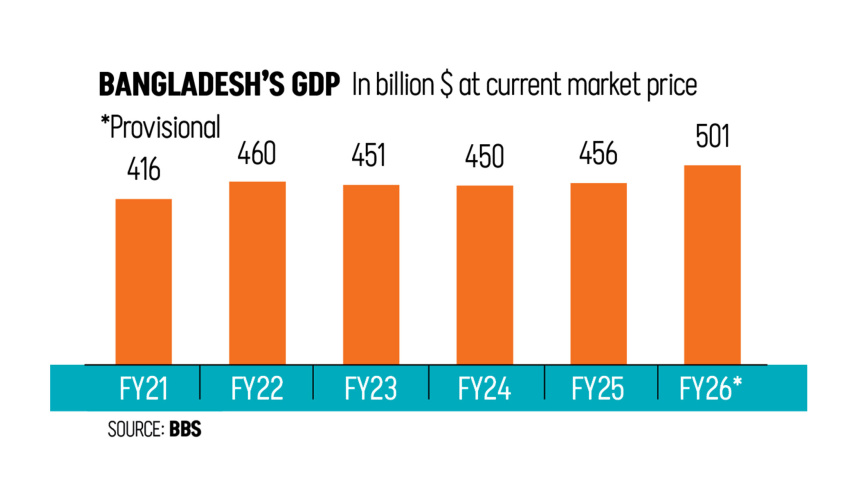

As per the current estimate, the gross domestic product -- a measure of the final value of goods and services produced in an economy over a given period -- stood at $501 billion this year, up from $456 billion a year ago. Per capita income rose to $3,020 from $2,769 the previous year.

Economists say the growth is a positive sign but stress that the government should prioritise macroeconomic stability before chasing higher growth through investment and productivity gains. They also warned that persistent price pressures could further squeeze fixed- and low-income earners.

“Bangladesh’s economy has been showing a trend of recovery, with the growth rate increasing. However, the extent of recovery has been quite moderate in comparison with the country’s historical record,” said Md Deen Islam, a professor of economics at Dhaka University.

“The most alarming factor in this regard is the relatively poor performance of its industrial sector,” he said.

According to the bureau, the agricultural sector expanded 2.78 percent in FY26, up from 2.42 percent a year ago, while services grew by 4.59 percent, up from 4.35 percent. Manufacturing, however, slowed to 2.86 percent from 3.71 percent as exports fell and domestic demand weakened amid persistent inflation.

In view of the above factors, the government’s goal of achieving 6.5 percent growth in the next fiscal year may be considered quite ambitious, said Professor Islam.

Though the provisional data show growth above 4 percent, the International Monetary Fund and other multilateral agencies had earlier forecast growth below that threshold for the year.

The Asian Development Bank attributed the slowdown in FY25 to political instability that weakened demand, compounded by labour disputes, recurring floods and restrictive macroeconomic policies, while elevated inflation persisted due to supply constraints.

Growth should gradually recover in FY26 and FY27 as consumption and investment pick up and political uncertainty fades with the general election out of the way, the ADB said. This, though, assumes that the Middle East conflict does not persist and global supplies normalise. The bank cautioned that rising interest payments and growing public debt levels warrant prudent debt management going forward.

To achieve the government’s growth goal, it will be necessary for economic growth to increase by more than two percentage points in one year, according to Prof Islam. To do this, there will be a need for a strong resurgence in private investments, higher exports, adequate energy availability, political stability, better credit flow to the productive sectors, and revival of domestic demand.

Although growth above 6 percent is possible, based on the present trend of the economy, which shows several obstacles such as high interest rates, stress on private investments, problems within the banking system, and economic uncertainties globally, he added.

A more realistic expectation for growth could be somewhere between 5 and 6 percent unless there is any change in the situation with respect to investments and industrial performance, Islam said.

The professor went on to note that if private investment becomes favourable, inflation falls and external pressures decrease, the level of growth would certainly pick up. “However, attaining the targeted 6.5 percent is certainly a distant possibility for the time being.”

Ashikur Rahman, principal economist at the Policy Research Institute of Bangladesh (PRI), said the government’s growth ambition is understandable and well-intentioned, but pursuing it through an expansionary fiscal and monetary policy mix carries serious risks given the current macroeconomic context.

Inflation remains close to 10 percent, export growth is weak, global uncertainty persists, the banking sector is under severe stress with non-performing loans reportedly above 32 percent, and the tax-to-GDP ratio barely reaches 7 percent, he noted.

“Against this backdrop, any attempt to stimulate growth through higher public spending and easier money could intensify inflationary pressures, worsen external imbalances and put renewed depreciation pressure on the exchange rate,” he said.

Such a course, according to him, would risk undermining the macroeconomic stability Bangladesh has painfully regained over the past two years.

“The priority, therefore, should not be to chase a headline growth number through demand-side stimulus. Instead, policymakers should focus on productivity-enhancing reforms that can raise potential growth without fueling instability,” said the economist.

This means deregulation, improving the investment climate, reforming and where appropriate privatising state-owned enterprises, strengthening the banking sector, and making critical investments in power, energy, logistics and infrastructure, he said.

Bangladesh should certainly aim for higher growth, but the path to that growth must be built on fiscal and financial sector reforms, productivity and confidence, not on policies that could reignite inflation and weaken macroeconomic stability, Rahman added.

Comments