Why inflation remains stubborn despite tighter monetary policy

“Excessive prices”

Few phrases have dominated public discourse in Bangladesh over the past several years as much as these two words. They have haunted households and policymakers alike.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. The impact is felt daily. Travelling a short distance by rickshaw in Dhaka for Tk 10 is a thing of the past. A bundle of leafy vegetables for Tk 10 requires hard bargaining with the floating vendor in neighbourhood alleys. Prices have risen so much that Tk 100 vanishes into a vegetable bag soon after it comes out of the wallet.

For a four-member family, keeping weekly bills for vegetables, eggs and other essentials within Tk 500 has become nearly impossible. That note now buys far less than it did two years ago. And there is no sign of prices cooling.

The Bangladesh Bank (BB) has maintained a contractionary monetary policy stance since the first half of fiscal year 2023-24 to make money more expensive and tame excess demand to curb inflation. It started raising the policy rate, or repo rate – at which it lends to commercial banks – in May 2022 and hiked it to 10 percent in October 2024. The rate is yet to come down.

Yet inflation – a measure of the increase in the prices of a basket of goods and services purchased by an average consumer – remains stubborn.

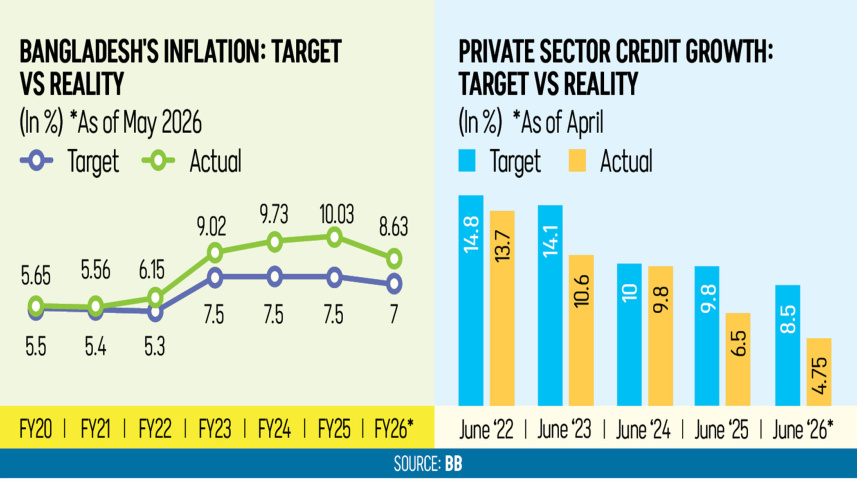

Month-on-month inflation stood at 9.42 percent at the end of May, with the 12-month average above 8.6 percent, indicating that overall inflation is likely to hover well above the BB’s target of 7 percent at the end of June this year.

This would be at least the sixth consecutive year inflation has exceeded the central bank’s targets. In FY25, average inflation hit 10 percent, more than 2 percentage points above target. The year before, it was 9.73 percent in June 2024, 2.23 percentage points above the BB’s goal.

Similarly, actual private-sector credit growth fell short of its targets set in the successive monetary policies.

In April 2026, it expanded by only 4.75 percent year-on-year, against a BB target of 8.5 percent by end-June. In April 2025, private-sector credit growth was 7.50 percent.

Public-sector credit growth, by contrast, exceeded its projected level.

The question is, why? What’s wrong with monetary policy that has failed to contain spiralling prices meaningfully, reverse sluggish demand and accelerate economic activity?

In its recent monetary policy statements, the BB attributed persistently high inflation to a combination of factors – the Russia-Ukraine war and conflicts in the Middle East, a more than 40 percent depreciation of the taka against the US dollar, and volatility in global commodity prices.

Domestically, years of a lending rate cap at 9 percent kept real interest rates negative for a while, repeated fuel and energy price hikes led to higher production and transportation costs, and government continued to borrow heavily to finance budget deficits.

This coincided with domestic production and supply disruptions caused by recurrent floods and rising inflation expectations, causing prices to trend upward.

FISCAL AND MONETARY FAILURES

Birupaksha Paul, professor of economics at the State University of New York at Cortland and a former chief economist at the BB, argues inflation has remained high “because of both fiscal and monetary failures.”

“The government has increased its borrowings to one of the highest levels, which is inflationary. On the other hand, the central bank’s liquidity support to cash-hungry banks is also inflationary. These two channels are thwarting monetary tightening with high policy rates,” he said.

The BB has so far provided Tk 75,903 crore in emergency liquidity assistance to banks facing cash shortages as of June 6, Finance Minister Amir Khosru Mahmud Chowdhury told parliament last week.

Meanwhile, the government’s net borrowing from the banking system surged more than threefold to Tk 1,04,410 crore during July–April of FY26, from Tk 30,405 crore a year earlier.

Birupaksha said high interest rates have also contributed to limited credit growth, while its weakness also stems from institutional failures such as non-inclusive politics, extortion by political thugs, and the poor law and order situation.

“The government failed to stimulate business confidence by adequately supporting the closed or vandalised mills and factories. It’s a new type of fiscal-monetary trap that adds fuel to inflation and delivers a damper to private credit growth,” he said.

INFLATION IS NOT DEMAND-DRIVEN

Fahmida Khatun, executive director of the Centre for Policy Dialogue (CPD), has a different reading.

She argues monetary policy has had limited success in achieving its key objectives for several reasons, primarily because inflation has not been driven by demand.

“Supply-side disruptions, exchange rate depreciation, higher import costs, and inefficiencies in domestic markets have all played a major role. Monetary policy, on its own, cannot easily solve this,” said Fahmida, also a director on the BB’s board.

For private-sector credit, she said high borrowing costs are only a part of the story. Weak investor confidence, energy shortages and policy uncertainty are also responsible.

“That is why we have seen earlier that when companies are reluctant to invest due to the lack of an enabling environment, simply adjusting interest rates is unlikely to generate the desired increase in private credit,” she said.

According to her, monetary policy should be supported by prudent fiscal policy and broader structural reforms that improve the investment climate, ease supply constraints, and strengthen market competition. “Without such policy coordination, bringing inflation under control while also stimulating investment and growth will remain a difficult balancing act.”

UNFAVOURABLE CIRCUMSTANCES

Deen Islam, professor of economics at Dhaka University, said the latest monetary policies of the BB failed to achieve their objectives not only due to the inadequacy of the policy rate but also owing to unfavourable circumstances.

“It should be noted that the rise in prices was caused mostly by supply-side factors, higher import prices, exchange rate effects, and market rigidity, whereas the banking sector was too weak to transmit policy signals effectively,” he said.

At the same time, private credit remained subdued because both banks and borrowers became cautious.

“Therefore, the next monetary policy should not only announce a rate stance; it should explain the transmission strategy: how BB will anchor inflation expectations, restore credit discipline, support productive lending, coordinate with fiscal policy, and rebuild confidence in the banking system,” he added.

Comments