Smaller investment rebates, bigger tax burden

The national budget and the finance bill are not merely statements of government income and expenditure; they are key policy instruments that shape the future direction of the economy. Tax measures not only generate revenue but also influence citizens' saving, investment, and consumption decisions.

Consequently, any change in tax benefits should be assessed as a policy decision rather than treated as a simple accounting adjustment.

For all latest news, follow The Daily Star's Google News channel.

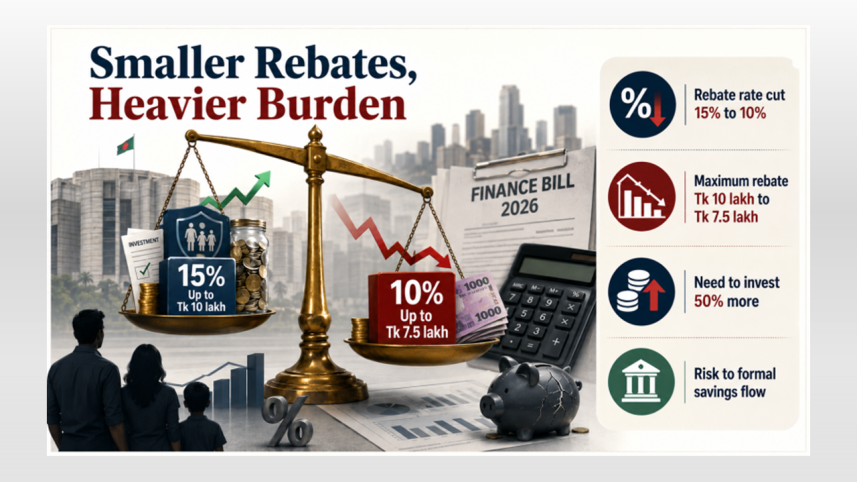

For all latest news, follow The Daily Star's Google News channel. The Finance Bill 2026 proposes a significant reduction in the investment tax rebate available to individual taxpayers. Under the existing system, the rebate is calculated as the lowest of three amounts: 3 percent of the taxpayer's total income eligible for rebate calculation, 15 percent of eligible investments and expenditures permitted under the law, or Tk 10 lakh.

The proposed bill would reduce the rebate on eligible investments and expenditures from 15 percent to 10 percent and lower the maximum rebate from Tk 10 lakh to Tk 7.5 lakh, while retaining the income-based ceiling of 3 percent.

Although these revisions may appear modest, they could substantially affect ordinary taxpayers by weakening incentives for household savings and investment. The proposed reduction therefore warrants careful reconsideration in view of its broader implications for individual financial behaviour and economic growth.

Consider a taxpayer whose total income for rebate purposes is Tk 10 lakh. Three percent of that income is Tk 30,000, which represents the maximum rebate available under the income-based limit. Under the current rules, the taxpayer must invest Tk 2 lakh in eligible instruments to obtain the full Tk 30,000 rebate because 15 percent of Tk 2 lakh is Tk 30,000. Under the proposed rules, the same taxpayer would have to invest Tk 3 lakh to receive the same rebate, since 10 percent of Tk 3 lakh is Tk 30,000. The required investment would therefore rise by Tk 1 lakh, or 50 percent.

Should the taxpayer continue investing Tk 2 lakh, the rebate would fall from Tk 30,000 to Tk 20,000. Assuming all other factors remain unchanged, the taxpayer's payable tax would increase by Tk 10,000. Thus, even without an increase in the formal tax rate, the effective tax burden would rise through the reduction in tax relief.

The two proposed amendments would affect taxpayers differently. Lowering the maximum rebate from Tk 10 lakh to Tk 7.5 lakh would mainly affect high-income taxpayers and those making large investments. Reducing the rebate rate from 15 percent to 10 percent, however, would affect a much wider group, particularly salaried and middle-income taxpayers.

For most salaried households, income is relatively fixed while living costs are not. After paying for food, housing, healthcare, education, transport, and other essentials, many families have limited capacity to save.

Inflation has already reduced purchasing power and placed household budgets under pressure. Expecting taxpayers to invest 50 percent more merely to retain the same tax benefit is therefore unrealistic for many middle-income families. The challenge becomes greater when funds must remain locked into long-term instruments.

A tax incentive is effective only when taxpayers have sufficient disposable income to use it. Where households cannot increase their investments, the proposed change will not necessarily encourage additional saving. Instead, it may simply place part of the existing rebate beyond their reach.

Investment tax rebates have traditionally encouraged people to save through life insurance, provident funds, deposit pension schemes, savings certificates, and eligible capital market instruments.

People do not save solely to reduce taxes, but tax incentives can help create regular, formal, and long-term saving habits. Weakening these incentives may lead some taxpayers to reduce or postpone investments. Others may keep their money in cash, informal arrangements, or less productive assets.

The result may not be a decline in total household savings but rather a reduction in the proportion of savings channelled through formal financial institutions and regulated investment vehicles.

This could have wider economic consequences. Savings deposited in banks, insurance funds, government savings schemes, and the capital market are converted into resources for business expansion, infrastructure, industrial development, and other productive activities.

A strong pool of domestic savings increases a country's ability to finance development and reduces excessive dependence on external borrowing and other forms of foreign financing. The relationship between tax rebates and savings is not automatic. Income levels, inflation, interest rates, investment security, and confidence in financial institutions also shape household decisions.

Nevertheless, tax rebates remain an important incentive for taxpayers with limited surplus income. Reducing that incentive at a time of prolonged pressure on living standards could adversely affect formal savings and long-term capital formation.

Bangladesh's low tax-to-GDP ratio is a serious and longstanding concern, and the government's need to raise additional revenue is undeniable. However, revenue mobilisation should not depend primarily on imposing greater burdens on taxpayers who are already registered, visible, and compliant.

A more sustainable approach would focus on bringing eligible individuals and businesses outside the tax net into the system. It would also require stronger measures against tax evasion and illicit financial flows, greater digitalisation of tax administration, effective integration of government databases, and a comprehensive review of unnecessary or poorly targeted tax exemptions.

Reducing benefits for compliant salaried taxpayers may be administratively convenient, but convenience does not guarantee fairness or sound economic policy.

If existing taxpayers see their incentives repeatedly withdrawn despite continued compliance, trust in the tax system may weaken. This could undermine voluntary compliance and send the wrong signal when the government is seeking to broaden the tax base.

Under the proposed amendments in the Finance Bill 2026, the tax rebate rate on eligible investments would be reduced from 15 percent to 10 percent, while the maximum rebate ceiling would also be lowered. Consequently, taxpayers would need to invest substantially more to receive the same level of tax benefit.

Before the Finance Bill 2026 is finalised, the proposed reductions in both the rebate rate and the maximum ceiling should be reconsidered. At a minimum, the government should assess their likely effects on middle-income households, formal savings, and domestic investment.

Revenue objectives can be pursued through a more balanced policy that protects lower- and middle-income taxpayers while encouraging productive, long-term saving.

Tax policy is not merely a mechanism for filling the public treasury. It also shapes economic behaviour. A policy that encourages citizens to save and invest while simultaneously reducing the incentives available to them is contradictory.

Sacrificing long-term capital formation for limited short-term revenue gains would not be a forward-looking policy choice.

The writer is a financial sector analyst and can be reached at faysal.aqc@gmail.com.

Comments